Why Homeowners Insurance Is Rising in the U.S.?

If you’re a homeowner, you may have noticed your insurance premium increase over the past few years. Many families across the state are asking the same question: Why is my insurance getting more expensive?

The answer isn’t just one thing. Several trends across the country — including rising building costs, more homes in risk-prone areas, and stronger weather events — are influencing insurance prices.

Understanding these changes can help Washington homeowners make smarter decisions about protecting their homes and finances.

This article is based on publicly available research and industry insights reported by Verisk Analytics, a company that studies risk patterns and insurance trends across the United States.

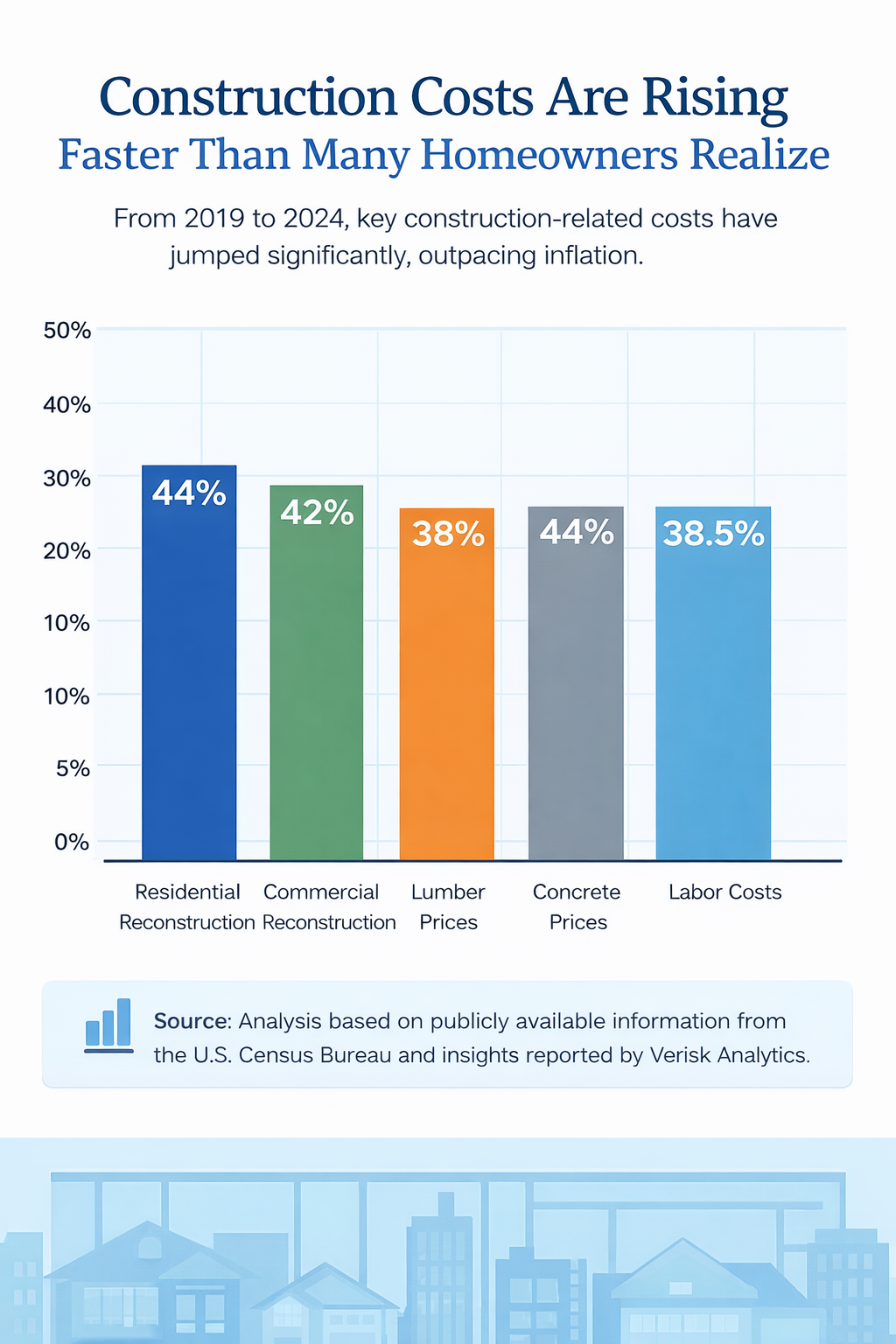

The Cost to Rebuild Homes Has Increased

Why This Matters in Washington

Washington has seen strong housing growth in recent years. When construction materials and labor become more expensive, the cost to repair or rebuild homes after damage also rises.

Because of this, insurance coverage limits sometimes need to be updated to reflect today’s rebuilding costs.

Weather Risks Are Changing

Washington State may not experience hurricanes like other parts of the country, but it still faces several natural risks that can impact homeowners.

These include:

- Winter windstorms

- Heavy rainfall and flooding

- Wildfires in Eastern Washington

- Earthquake risk along the Cascadia Subduction Zone

Across the United States, extreme weather events have become more frequent and more costly. Research referencing insights from Verisk Analytics shows that losses from wind and severe storms have more than doubled when compared to recent years to previous decades.

When disasters cause more damage, insurance claims increase — which can influence premiums over time.

Population Growth in Risk Areas

Another trend affecting insurance costs is where people choose to live.

Across the country, more homes are being built in areas exposed to wildfire risk, storms, or other natural hazards.

This trend also affects parts of Washington where communities are expanding into forested or rural areas that may face wildfire exposure.

When more homes are in areas with higher natural risk, the potential cost of disasters increases.

Other Factors That Affect Insurance Costs

While rebuilding costs and weather risks play a major role, other factors can also influence insurance prices.

These include:

- Insurance fraud, which adds billions of dollars in costs each year

- Legal expenses related to claims and lawsuits

- Inflation affecting construction materials and labor

All these elements contribute to the overall cost of protecting homes and paying claims when damage occurs.

What Washington Homeowners Can Do

Although many of these trends are outside of a homeowner’s control, there are steps you can take to make sure your home is properly protected.

Review your policy regularly

Coverage should reflect today’s rebuilding costs.

Work with a local independent insurance agency

Independent agencies can compare multiple insurance companies and help find the right coverage.

Ask about safety improvements

Upgrades like newer roofs, smoke detectors, or wildfire-resistant landscaping may qualify for discounts.

Make sure your coverage is current

Keeping your policy updated helps reduce the risk of being underinsured after a loss.

~Final Thoughts~

Insurance is designed to help homeowners recover financially after unexpected damage.

As construction costs and weather risks continue to evolve, reviewing your coverage periodically can help ensure your home remains properly protected.

Research from Verisk Analytics shows that these trends are influencing insurance costs across the country — including here in Washington State.

Staying informed and working with a knowledgeable local advisor can help you navigate these changes with confidence.

Source: Analysis based on publicly available data from the U.S. Census Bureau and insights reported by Verisk Analytics.